Tired of renting? Find out the pros of buying a house in today’s market and how it could save you money and broaden your future buying potential.

With rents spiking across the country, Australians are once again asking themselves: is this a good time to buy a house? Buying or building a new home requires an initial outlay of money. If you can come up with a deposit, though, it can mean serious savings down the track as well as many home owner benefits. Here are five reasons why buying an established or new home can save you money.

There are many hidden costs to renting! Here we break down the five reasons why this is a good time to buy a house and how it might be more cost-effective in the long run.

There are many hidden costs to renting! Here we break down the five reasons why this is a good time to buy a house and how it might be more cost-effective in the long run.

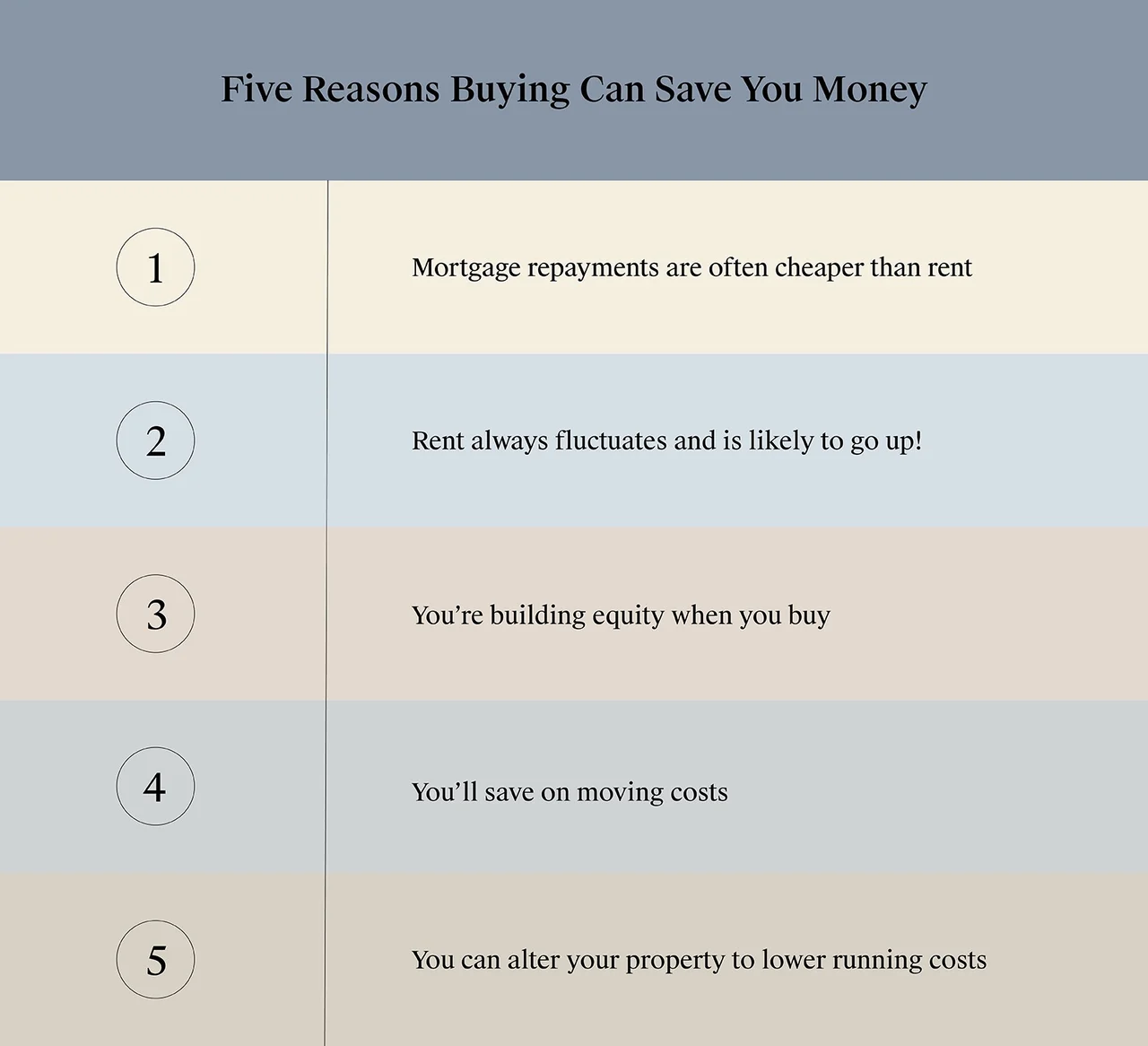

1. Mortgage repayments are often cheaper than rent

Analysis from realestate.com.au shows that buying is cheaper than renting for 56.8% of Australian homes. This won’t surprise those who pay more in rent each week than they would in mortgage repayments for a comparable property. The study also factors in ‘hidden costs’ like rates, taxes, and maintenance, which landlords cover during tenancy.

Buying tends to be more affordable in regional areas and the outer suburbs of major cities. Renting, however, is generally cheaper in inner-city locations—especially in Sydney and Melbourne.

In Victoria, the five suburbs where buying is cheapest compared to renting are:

- Waterford Park

- Rockbank

- Mickleham

- Milgrove

- Wollert

Rents keep rising—making a flexible home loan an attractive option that could help you save on mortgage repayments in the long run.

Rents keep rising—making a flexible home loan an attractive option that could help you save on mortgage repayments in the long run.

2. Rent always goes up

In the first year of homeownership, mortgage repayments typically account for about 26% of your salary.

Once your loan is secured, however, there’s a cap on how much repayments can increase. If you have a variable rate loan, interest rate rises may raise your minimum repayment, but only within a manageable range. For instance, a 1% interest rate increase on a $650,000 mortgage would add roughly $400 per month—or about $100 per week. Making extra repayments on your loan principal can reduce this amount even further.

On the upside, wage growth and natural inflation mean that over time, your mortgage payments will become a smaller portion of your income. After 20 years, the average mortgage payment drops to just 15% of income. Meanwhile, renters face rent increases tied to inflation; in fact, during 2021/22, rental prices in capital cities surged by 14.7% in just one year due to a tight rental market.

Get a clearer picture of your current rental costs versus buying potential with our Rent V’s Buy Calculator

How can equity save you money? Here are a few ways:

First, if you’re a first-time buyer who purchased with less than a 20% deposit, you probably paid lenders mortgage insurance (LMI). But you don’t have to wait until you’ve paid down a large portion of your loan to eliminate this extra cost. As your home’s value rises, your loan becomes a smaller percentage of that value. For example, if you bought a house and land package for $800,000 with an $80,000 deposit and a $720,000 loan, your loan-to-value (LTV) ratio starts at 90%. Over time, as property values increase, your LTV decreases. Many lenders allow you to cancel LMI once your LTV drops to 80% or below, saving you thousands.

Second, building equity opens up more options. If you initially purchased with a minimal deposit, you might not have access to the full range of home loan products. As your equity grows, lenders see you as less risky, which could mean better loan terms or lower interest rates. It’s a good idea to reconnect with your mortgage broker to see if switching lenders or refinancing could benefit you.

4. You’ll save on moving costs

Renting in Australia often comes with housing instability. According to Australia Post data, renters typically move once every four years, usually staying within the same suburb. However, this data doesn’t fully capture the post-pandemic rental market, where available rental properties have significantly decreased, and many are being converted into short-term accommodations. As a result, some tenants are now moving every year—or even more frequently.

Moving always comes with costs: removalist fees, storage charges if there’s a gap between homes, utility connection expenses, mail redirection, and often the cost of a professional cleaner at the end of a lease. The more frequently you move, the more these costs add up. Buying a home gives you the stability to stay put—and the freedom to move only when you want to.

One of the biggest advantages of homeownership is the freedom to make cost-saving improvements and energy-efficient upgrades—options that renters often don’t have. As a homeowner, you can customise your space with endless possibilities to reduce bills and boost comfort.

One of the biggest advantages of homeownership is the freedom to make cost-saving improvements and energy-efficient upgrades—options that renters often don’t have. As a homeowner, you can customise your space with endless possibilities to reduce bills and boost comfort.

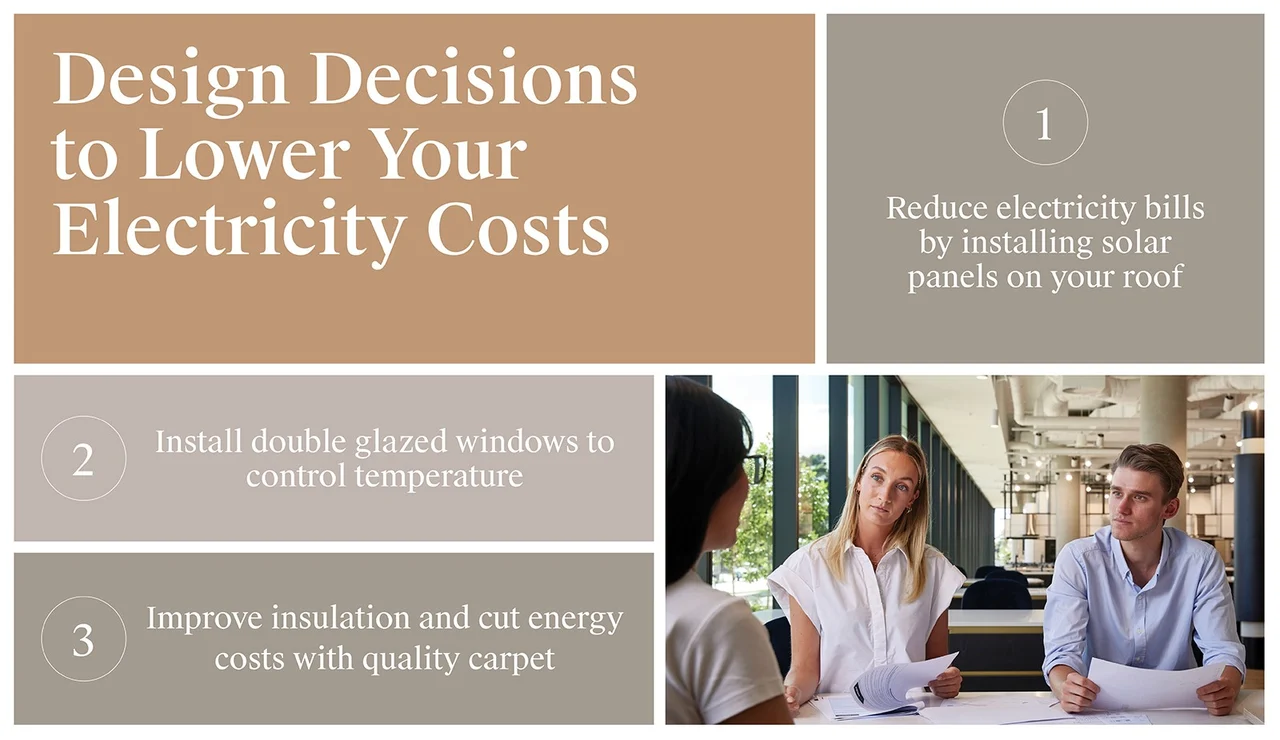

5. You can alter your property to lower running costs

Owning a home does come with maintenance costs, but it also gives you the freedom to manage and reduce those expenses. For example, installing solar panels can lower your electricity bills over time, while double-glazed windows help cut winter drafts and maintain a consistent temperature year-round. Even upgrading to quality carpet can make a noticeable difference in comfort and energy efficiency.

As a tenant, you might not have the ability to make these improvements or upgrade heating and cooling systems to more efficient models, which can lead to higher utility bills compared to homeowners.

After years of rapid, unsustainable growth, prices are adjusting to a more stable and sustainable pace. This reset is promising news for homebuyers looking at the long term.

Meanwhile, demand for outer suburbs and undeveloped land remains strong. These more affordable markets are proving more resilient than established inner suburbs, suggesting that buying now could mean your property will continue to grow in value over time.

With the market balancing out and high demand for new land, now is a great time to buy a home. Plus, the many benefits of homeownership can help you save money now and well into the future.